President Obama and his new government have adopted a series of measures to deal with the financial crisis. We have expectations as to the effects of these measures. We have lent a huge amount of money to the U.S. Of course we are concerned about the safety of our assets. To be honest, I am definitely a little worried.

While the announcement represented political posturing (to an increasingly restless, domestic Chinese audience), it should nonetheless be heeded as a warning, that the US cannot expect China (and other foreign Central Banks) to fund US budget deficits indefinitely.

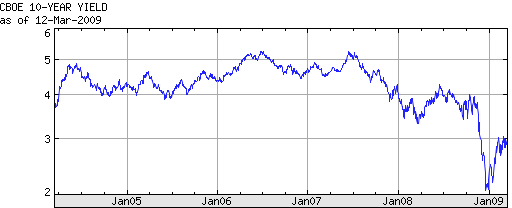

Let’s put aside the rhetoric for a moment, and examine the data. This week witnessed strong demand for Treasury securities, which were auctioned by the Treasury Department on consecutive days. Despite historically low yields (see chart), investors continue to snap up Treasury Bonds, mainly for the sake of risk aversion. The newly-revived issuance of 30-year bonds also went off without a hitch, and were more than 2x oversubscribed. Most relevant to this discussion is the fact the foreign Central Banks accounted for as much as 46% of demand!

The most recent Federal Reserve Statistical Release paints a similar picture. While foreign Central Banks and other international institutions reduced their holdings of US government securities slightly from the previous week, the decrease was essentially negligible. Overall, such entities have increased their holdings by at least $440 Billion over the previous year, bringing the total to approximately $3 Trillion (depending on the data source). China’s contribution remains substantial. Of its $2 Trillion in foreign exchange reserves, “Economists say half of that money has been invested in United States Treasury notes and other government-backed debt.”

However, there are a few reasons why I don’t think this trend will continue. First of all, the buildup in foreign Treasury holdings that transpired over the last decade was largely a product of unsustainable global economic imbalances, as net exporters to the US invested their perennial trade surpluses in what they perceived to be the world’s most secure investment. Temporarily putting aside whether Treasuries are actually secure, economic indicators suggest that Central Banks simply do not have the capacity to increase their holdings by much more. China’s trade surplus plummeted to $4.8 Billion last month; one economist projects a surplus of only $155 Billion in 2009, compared to nearly $300 Billion in 2008.

You can also remove from the list Japan- the second-largest holder of US Treasury securities- which is now running a trade deficit. Instead, both countries have publicly announced plans to use some of their forex reserves to fund domestic economic initiatives.

Then there is the equally unsustainable short-term buildup in US Treasuries, which is largely a product of technical factors. As I mentioned above- and which should be clear to all investors- the current theme underlying securities markets is one of risk aversion. In fact, it now appears that a bubble is forming in the bond market, and “any exodus now could spark selling across the board. Foreign debt holders would likely repatriate their funds immediately to reduce the risk of being last to convert.” As soon as markets recover- of which there are already nascent indications- investors will probably reduce their holdings of government bonds, or at least not increase their holdings.

Even the most conservative projections indicate a cumulative budget deficit for the next few years measuring in the the Trillions. Unless the risk-aversion theme obtains for the next decade, it seems unlikely that foreigners can be tapped to fund more than a small portion, leaving the Federal Reserve (with the help of its printing press) to make up the shortfall.

No comments:

Post a Comment